SMM September 26: As the end of September approaches, China's National Day and the traditional Mid-Autumn Festival are drawing near. According to the General Office of the State Council's "Notice on the Arrangement of Some Public Holidays in 2025," the National Day and Mid-Autumn Festival holidays will span eight days, from Wednesday, October 1 to Wednesday, October 8.

With less than a week to go before the National Day & Mid-Autumn Festival holiday, major lead-acid battery enterprises are gradually arranging pre- and post-holiday work schedules. Based on SMM's survey of holiday plans among various lead-acid battery enterprises across eight provinces in China, most enterprises plan to take 2–5 days off during the 2025 National Day holiday. Some enterprises will not take any leave or will take 6–8 days off, while a few plan holidays of up to 15 days.

By segment, demand in the e-bike battery market remains moderate. In particular, the implementation of the new national standard for e-bikes in September, which raised the maximum vehicle weight to 63 kg, has driven a corresponding increase in demand for lead-acid batteries. Coupled with the replacement of old vehicles, orders for complete vehicle supporting batteries have improved for lead-acid battery enterprises. As a result, some enterprises plan to take shorter holidays or no holiday at all, while most others will take 2–5 days off.

In contrast, demand in the automotive lead-acid battery market has been relatively weak. On one hand, the share of NEVs in vehicle usage continued to grow this year (according to CAAM data, NEV sales accounted for 48% of China's total domestic auto sales from January to August 2025, and this figure is expected to reach 50% for the full year of 2025). The substitution of lithium batteries for lead-acid batteries has also increased. On the other hand, due to the widening ratio between domestic and international lead ingot prices and changes in tariff policies, export-oriented automotive lead-acid battery producers have seen weaker orders. Many producers plan to extend their holiday periods, ranging from 3–5 days to 6–8 days. A few enterprises have even started their holidays this week, lasting until the end of the National Day holiday, for a total of about half a month.

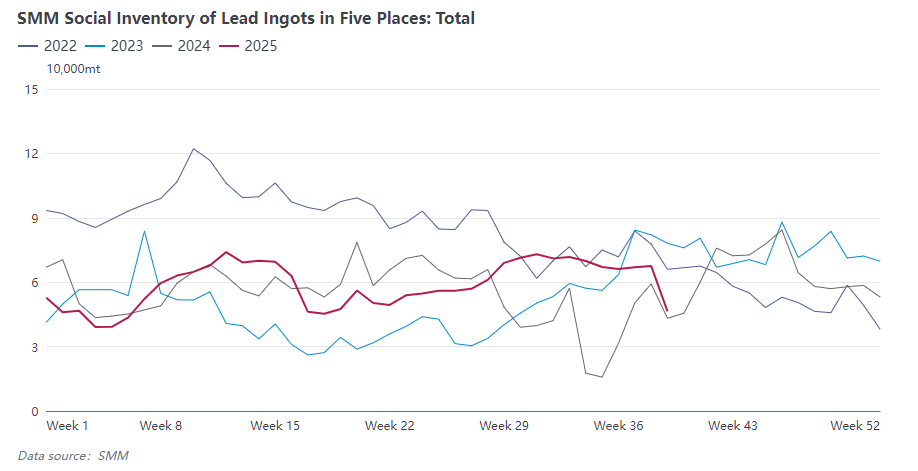

Additionally, orders for ESS battery enterprises remained relatively stable, leading to slightly shorter holiday periods. However, export-oriented enterprises in this segment generally plan slightly longer holidays, typically ranging from 0 to 5 days. Additionally, compared with the same period in 2024, major lead-acid battery enterprises had shorter holiday breaks this year, while export-oriented automotive lead-acid battery companies experienced longer holidays. As a result, lead-acid battery manufacturers showed mixed performance in lead ingot stockpiling ahead of the National Day holiday. Some enterprises did not conduct pre-holiday stockpiling as existing inventories were sufficient for production, while several large companies carried out nearly three weeks of pre-holiday stockpiling, leading to significant destocking of lead ingots before this year's National Day holiday. According to the latest SMM data, social inventories of lead ingots dropped by over 20,000 mt this week to 46,400 mt, hitting a four-month low. In contrast, during the same period last year, social inventories of lead ingots showed an inventory buildup before the National Day holiday. Certainly, the substantial destocking of domestic lead ingot inventories before the holiday this year was not solely due to pre-holiday stockpiling by lead-acid battery enterprises. Another contributing factor was maintenance or production cuts at multiple secondary lead enterprises in September, coupled with maintenance at some primary lead smelters. The combination of supply reductions and front-loaded consumption drove this outcome.

Data Source Statement: Data other than publicly available information is processed by SMM based on public information, market communication, and SMM's internal database model, and is for reference only, not constituting decision-making advice.